1Q23 Letter: "Volatility Remains Elevated and Downside Risks Persist"

To get our market insights delivered directly to your inbox, sign up here.

Business Update

During the first quarter of 2023, Evolve Investing continued its growth trajectory. We added several new clients and our assets under management increased by 15% from the end of 2022, to an all-time high. To better support our clients, Evolve Investing is hiring a Client Services Associate. A full description of the role is available via this link, and I welcome any introductions to ideal candidates.

It’s been a challenging last twelve months for the economy, the banking system, and the financial markets. As your advisor, my goal is to help you navigate short-term challenges while focusing on your long-term goals for wealth creation. As always, you’re welcome to reach out to me directly anytime to discuss the markets and your investments.

Reflections on 1Q23

The first quarter of 2023 was absolutely one to remember. We entered the year anticipating a near-term economic slowdown. An unexpected blow to the economy followed, with the failure of Silicon Valley Bank (SVB). As the SVB failure shattered investor confidence and introduced concerns over systematic risks to the banking industry, we saw meaningful declines in equity valuations across the financial sector, with regional banks hit particularly hard.

S&P Regional Banking ETF vs. MSCI World Net Total Return, 1Q23

Despite these headwinds, stocks and other risk assets generally had a strong quarter. Specifically, the Dow Jones Industrial Average ended the quarter up 0.4%, the S&P 500 rose 7% during the quarter – the best three-month stretch since 4Q21 – and the Nasdaq Composite gained 16.8% as investors perceived technology stocks as a “safe haven” amid financial sector turmoil.

S&P 500, Nasdaq 100, and Bloomberg Aggregate Index Return, 1Q23

Outlook for 2023

The speed of the bank run on SVB’s deposits was unprecedented; within 48 hours of the bank disclosing its intentions to raise capital, it was insolvent. Given the known ease with which customers can withdraw cash, bank deposit balances now feel less stable than they did prior to SVB’s failure. As a result, I expect various banks to curtail lending as they shore up liquidity. A slower pace in lending activity generally means slower economic activity.

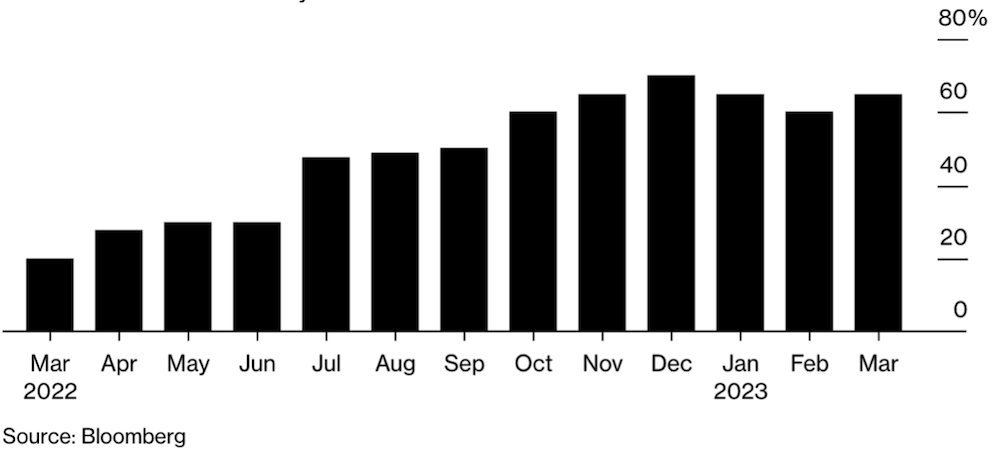

Echoing my sentiments from last quarter, I continue to believe that a near-term economic slowdown is likely. Following the SVB crisis, a recent Bloomberg poll of 48 economists now suggests a 65% chance of recession, up slightly from 60% odds in February and down slightly from 70% odds at December 2022.

Probability of a U.S. Recession in 2023

In light of persistent recession fears and banking sector woes, the Federal Reserve is now tasked with considering not only slowing economic growth, but also tightening financial conditions when making policy decisions. In its most recent policy statement, the Fed noted that “some additional policy firming may be appropriate,” a contrast to their earlier reference to “ongoing increases” as noted in December.

Generally, I now see a higher probability that the Federal Reserve and other central banks will end their rate hiking cycles sooner than later. Further supporting this expectation is last Friday’s release of the core personal consumption expenditures price index, which was up 4.6% y/y in February, a slowdown from 4.7% y/y in January. The data came in slightly below economists’ consensus expectations.

U.S. Personal consumption expenditures (PCE) and Core PCE, Annual Growth

How We’re Positioning

Last quarter I shared that I was generally cautious regarding growth stocks. My view is unchanged; I continue to prefer less interest rate sensitive areas of the stock market such as healthcare, consumer staples, and utilities. While equities remain a key component of our long-term positioning, most of our strategies are currently underweight stocks relative to other assets.

In turn, I have increased allocations to fixed income securities, including government and corporate bonds as well as senior secured loans. Not only are bond yields more attractive than they’ve been in years on an absolute basis; my expectation is that we could see capital appreciation among bonds in the event of a deeper than anticipated economic slowdown. Importantly, the “equity risk premium” for stocks relative to bonds is currently at 10-year lows.

10 Year Treasury Yield vs. S&P 500 Earnings Yield

Within the fixed income category, I continue to like BB-rated bonds with effective yields in excess of 7.0%, and relatively low default rates within the high yield category.

Final Thoughts

Generally, my expectation for the balance of 2023 is that confidence will remain fragile while volatility will remain elevated. My current strategies remain oriented to this perspective, with a bias toward managing downside risk.

Please reach out anytime to discuss any of the above themes and how your portfolio is positioned. Thank you for your continued support and confidence in Evolve Investing.

Best,

Peter Hughes, CFA, CEPA®