1Q25 Letter: "Turning Point"

From Rhetoric to Reality: Broad Tariffs Take Hold

In a conversation last year, veteran investor Howard Marks summed it up well: “Probably 98% of the things Trump will do can’t be predicted, and even the consequences of the things we know he’ll do probably can’t be predicted.”

That sentiment has rung especially true in recent weeks. Just a few months ago, I shared my view that broad-based tariffs floated by the Trump campaign were more likely a negotiation tactic than actual policy. At the time, markets appeared to agree, having largely priced in existing tariffs, and I believed the potential for tax cuts and deregulation might outweigh those risks.

But I’ve been surprised by how quickly and definitively those threats have materialized. Last week, President Trump announced a new round of sweeping import tariffs, with broad and aggressive terms. A minimum 10% tariff will apply across all imports to the U.S., with country-specific increases that mark a clear escalation in trade policy:

The European Union faces a 20% tariff

Japan will see a 24% levy

China, the most frequent target of these policies, will be hit with an even higher rate

For decades, low-cost imports have helped hold down inflation and support Americans’ standard of living. Broad new tariffs, along with retaliatory measures from other nations, risk reversing that trend and slowing global economic integration – and potentially reintroducing inflationary pressures at a time when the Federal Reserve is still seeking clarity on when to begin cutting interest rates.

Until recently, the Federal Reserve appeared on track to engineer the elusive “soft landing”—guiding inflation back to its 2% target without tipping the economy into recession. Markets had begun pricing in a measured path of interest rate cuts as growth cooled just enough to keep inflation in check. However, Fed officials are now on pause, caught between the risk of slowing growth from trade disruptions and the potential for higher consumer prices. This dynamic could lead to stagflation: a rare but difficult economic environment where inflation remains high even as growth slows and unemployment rises.

Equity Volatility, Credit Opportunity: Repositioning with Discipline

The breadth and severity of President Trump’s new tariff announcement caught most economists and market analysts off guard. What had previously been considered political posturing quickly turned into concrete policy, with sweeping implications. Analysts at Morgan Stanley and Barclays now estimate that the effective U.S. tariff rate could rise as high as 20-22%—a significant jump from the prior baseline of 8–9%.

On the Thursday following the announcement, the S&P 500 fell 4.8%, the Dow Jones Industrial Average dropped 1,679 points (or 4%), and the Nasdaq Composite tumbled 6%—its worst single-day decline since March 16, 2020, in the early days of the COVID pandemic. The message from markets was clear: renewed trade friction and policy uncertainty are meaningful risks, and the narrative of a soft landing and steady easing has been materially disrupted.

This doesn’t mean equities are no longer worth holding, but it does warrant a fresh look at asset allocation. The majority of our clients hold portfolios that contain stocks, bonds, cash alternatives, and in some cases short positions and commodity hedges. We maintain a strategic allocation to align risk with our clients’ time horizon, cash flow needs, and capacity to stay invested through uncertainty.

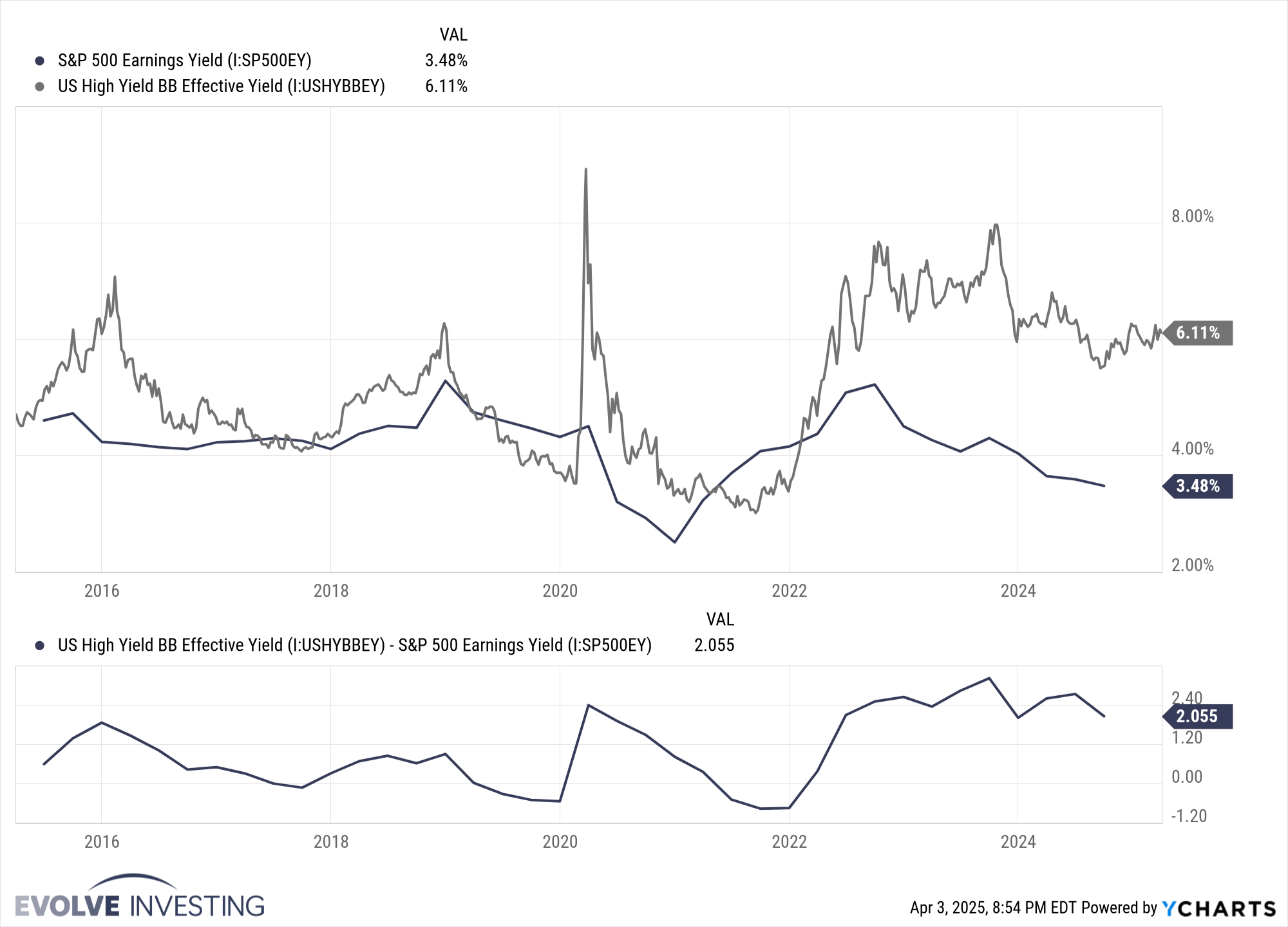

Even before this shock, we had highlighted the relative value between stocks and bonds—and credit continues to stand out. Even with Thursday’s selloff, the yield on the 10-year U.S. Treasury note is higher than the “earnings yield” on the S&P 500 stock index. (The earnings yield is the ratio of earnings to price, the inverse of the p/e ratio.)

10 Year Treasury Rate vs. S&P 500 Earnings Yield

Despite narrower spreads, current yields in high-quality and crossover credit remain compelling, particularly when viewed through the lens of risk-adjusted return. These are returns that are contractual and far less vulnerable to shifting political winds or market sentiment, although they are subject to default risk.

For income-focused clients, we continue to favor BB-rated corporate bonds, short-dated governments, and investment-grade corporates. In BBs especially, the spread between their effective yield and the earnings yield of the S&P 500 remains attractive. This gives us a way to capture income with less volatility than equity exposure in the current environment.

BB Effective Yield vs. S&P 500 Earnings Yield

To be clear, this is not a shift away from equities—we remain long-term investors. While we’re emphasizing risk management and relative value, some clients with higher risk tolerance have used the recent market pullback as an opportunity to selectively add equity exposure. In the right context, volatility can present attractive entry points, particularly for those with a long time horizon and the ability to stay invested through continued uncertainty.

Our focus remains on balancing risk and reward, and tailoring strategies to meet each client’s unique goals as the environment evolves. We aim to build resilient portfolios—designed to navigate uncertainty without overreacting to it. In periods like this, discipline, clarity, and a long-term perspective matter more than ever.

As always, we welcome a conversation if you’d like to discuss any of the themes above or revisit how your portfolio is positioned. Thank you for your continued trust and confidence in Evolve Investing.

Best,

Peter Hughes, CFA, CPWA®, CEPA® & Chris Stevenson, CFA