2023 Outlook Letter

To get our market insights delivered directly to your inbox, sign up here.

Reflections on 2022

In January of last year, I wrote that I was feeling optimistic about 2022. That sure turned out to be a case of wishful thinking. And it also highlights how quickly the world can change.

At this time last year, the Federal Reserve had not yet announced an official rate hike, and inflation was tracking closer to 7%, compared to a recent peak of 9% in June 2022. There was no consensus view as to whether or not Vladimir Putin really would invade Ukraine, or whether COVID would resurge in China and impact its economy. These last two factors worsened the inflation picture meaningfully, which forced the Fed to raise rates faster and more aggressively than previously anticipated.

This meaningful policy shift by the Federal Reserve to a more hawkish stance drove a selloff of all risk assets. Stocks closed out 2022 with their worst year since the 2008 financial crisis. The S&P 500 ended the year down 19.4%, its fourth-worst decline on record since its inception in 1957. The tech-heavy NASDAQ was down 33%, and blue-chip technology stocks including Alphabet Class C stock, Tesla, and Meta Platforms had their worst year on record. Bitcoin and Ethereum were down 64% and 67%, respectively, for the year.

Like many investors, I was surprised by these shocks to the global economy. While my portfolios benefitted from a bias toward value stocks and away from growth stocks, particularly high-growth technology stocks, they were not immune to broad market movements. In the first quarter of 2022, I eliminated European stocks from my portfolios and implemented commodity hedges, where appropriate. Later in the year I allocated several portfolios to a generally higher percentage of bonds and cash, where appropriate.

In my last letter I wrote that it is nearly impossible to “time the market,” and no professional money manager has proven their ability to do so over time. As an advisor, I add value by shifting between more defensive and aggressive positioning as the overall investment environment changes, while also considering each individual’s unique level of risk tolerance. While I had expected a better year for the markets, I am generally pleased with how my portfolios performed relative to major market benchmarks.

Fundamental Outlook for 2023

As we enter 2023, I continue to believe that a near-term economic slowdown is likely. This outlook is unchanged from my views in October, April and in July. I am not alone in my view, as a recent Bloomberg poll of 38 economists suggests a 70% chance of recession.

Probability of a U.S. Recession in 2023

There are a number of factors driving this economic slowdown. Higher borrowing costs are weighing on the housing market. Consumers’ savings account balances have declined from post-pandemic levels. And there is a broad negative wealth effect from lower valuations in bonds, equities, private investments, and crypto.

While I acknowledge these factors, I continue to anticipate a mild recession for the following reasons:

Roughly two-thirds of the U.S. economy is consumer-driven, and consumer spending has remained resilient. According to a recent Federal Reserve Survey, consumers are expecting to spend at elevated levels in 2023, albeit below the peak levels reported in early 2022.

U.S. Household Spending Growth Expectations by Income Level

Even with excess savings now largely depleted, U.S. households’ balance sheets remain strong. As a percentage of disposable personal income, net worth of households is at a historically favorable level. Roughly 65% of household debt is mortgage debt and is mostly held by higher-quality (prime) borrowers as a result of the tightening of lending standards following the Financial Crisis of 2008.

Household Wealth as a Percentage of Disposable Personal Income

Consumer price inflation appears to be moderating. Recent data from the Labor Department showed that the core consumer price index, which excludes food and energy, was up 0.2% month-over-month in November 2022 and was up 6% from a year earlier. November’s data marked the smallest monthly advance in 15 months, suggesting that inflation is moderating.

Wage inflation appears to be moderating.In December 2022, average hourly earnings rose 0.3% from October and 4.6% y/y, suggesting that inflationary pressure in wages is moderating.

Consumer Price Index and Average Hourly Wages, Last 5 Years

How We’re Positioning

While each of my portfolios are customized to my individual client’s preferences, several themes are emerging as I position for 2023:

As a result of last year’s violent market selloff, the price-to-earnings multiple of the S&P 500 declined as much as seven times from its post-pandemic peak, while stocks in more speculative growth segments of the market were down 70-80% from highs. Despite this favorable reset in valuations, I continue to remain cautious regarding more interest rate-sensitive parts of the equity market. My preference remains generally defensive, with lower technology sector exposure relative to major benchmarks.

S&P 500 Price to Earnings (P/E) Ratio, Trailing and Estimated

I continue to expect the U.S. to fare better relative to other developed economies, and my strategies remain squarely focused on U.S. stocks at this time.

To repeat my thoughts from my April 2021 letter, the low-interest rate environment that characterized the 12-year period following the financial crisis is over, and investors are now adapting to higher real yields and nominal yields. I'm seeing increasingly attractive opportunities in select corporate investment-grade and high-yield bonds.

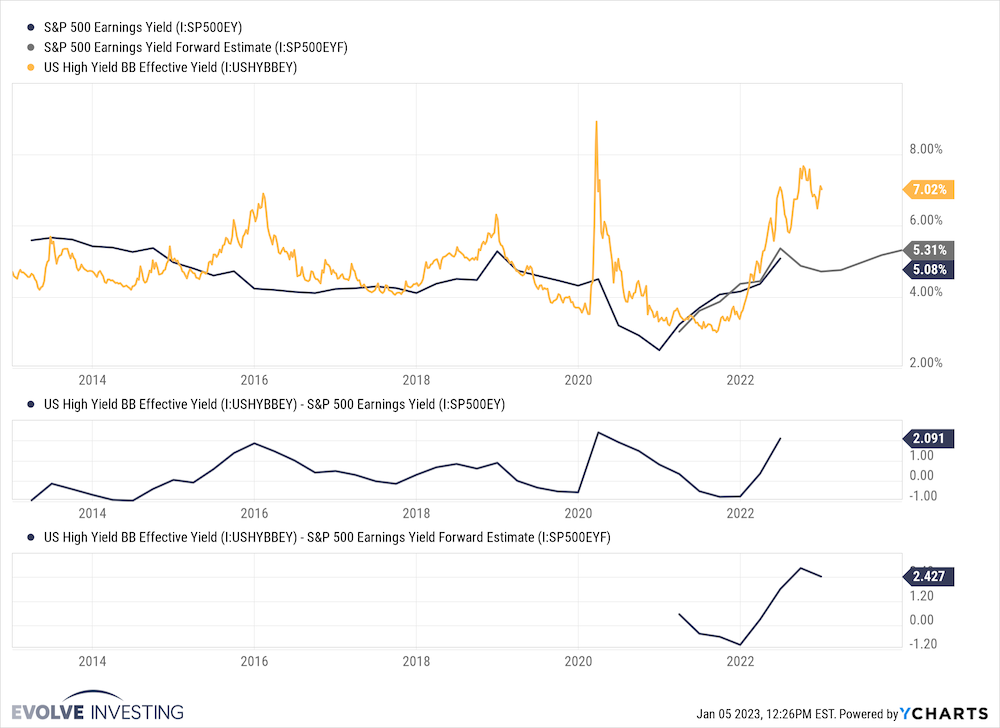

Within the high yield bond category, I find BB rated bonds to be attractive with effective yields in excess of 7.0%. As shown in the chart below, the spread between the effective yield on BB rated bonds and the earnings yield on the S&P 500 is the widest it’s been in over 10 years.

BB-Rated Bond Effective Yield vs. S&P 500 Earnings Yield

Importantly, BB-rated bonds tend to have lower overall risk of default compared to the overall high yield category.

Descriptive Statistics On One-Year Global Default Rates

For portfolios that prefer a lower-risk, shorter-duration strategy, I continue to like short-term treasury bonds.

Final Thoughts

The last year was challenging and humbling for all investors, including myself. While I have no crystal ball, I offer a few observations:

A 2023 recession is a foregone conclusion at this point. Any upside to that expectation would likely be supportive for all risk assets.

I believe that markets are forward-looking, and I would bet that stocks bottom before the recession concludes.

Since 1928, the S&P 500 Index has only fallen for two straight years on four occasions: The Great Depression, World War II, the 1970s oil crisis, and the dot-com bubble burst.

I believe investor sentiment is at a multi-year low. In my experience, lows in investor sentiment tend to coincide with lows in the markets.

As your advisor, my goal remains to position your portfolio for upside in the event of more favorable outcomes relative to consensus expectations, while also mitigating downside risk. Please reach out anytime to discuss any of the above themes and how your portfolio is positioned. Thank you for your continued support and confidence in Evolve Investing.

Best,

Peter Hughes, CFA