3Q21 Letter: “Looking Toward the Future”

Business Update

During the third quarter, Evolve Investing continued its growth trajectory. Specifically, we added several new clients and our assets under management grew by over 50% from the end of June. To better support our clients, we have deepened our analytical resources, expanded our team, and enhanced our impact methodology to include causes such as disease eradication, clean water access, supporting healthy oceans, and ending hunger.

As I look toward the future, I am compelled to maximize the time and energy directed toward Evolve Investing’s mission to create a regenerative, more just, and healthier world. To that end, I have made the decision to step back from my performance and life coaching practice to focus exclusively on Evolve Investing.

I am excited about the opportunities we can create to help our clients learn about and angel invest into early-stage, impact-oriented companies. As Evolve Investing continues to grow and expand, I welcome any introductions to early-stage founders and impact investors aligned with our mission.

Climate & Green Investing Update

In early August, the UN Intergovernmental Panel on Climate Change (IPCC), a working group comprised of 195 countries, released its first report since 2013. The IPCC concluded that “it is unequivocal that human influence has warmed the atmosphere, ocean and land,” and that the consequences of climate change are observed globally.

This report couldn’t have come at a more appropriate time. Relative to 2013, we are seeing far more of the effects of climate change in our daily lives. This trend was highlighted by the deadly heatwave that recently gripped the northwestern U.S. and British Columbia and was found to be directly linked to greenhouse gas pollution.

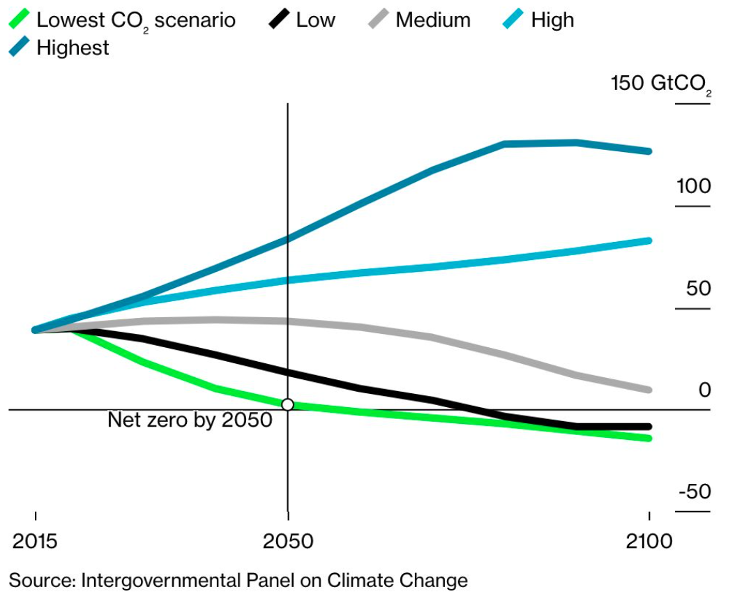

A key piece of data in the IPCC report is the revision to a range of estimates for global temperature increases resulting from human activity. The IPCC now expects temperatures to rise 2.5-4°C, a much smaller range than 1.5-4.5°C outlined in prior reports. This revision is particularly important because the previous 1.5°C low end of the range – which has since been eliminated – had been viewed as having a mild effect on the environment. The takeaways are that we’ll inevitably feel the impact of climate change, the consequences of our actions will likely get worse, and concerted action is necessary to prevent catastrophe.

As an investment advisor, I feel more compelled than ever to direct capital to companies that are taking steps to make a positive impact on our environment, and I believe that doing do mitigates risk in my clients’ portfolios. By investing more heavily in companies that have shorter-term targets to be carbon neutral, we create portfolios that are more resilient to actions such as increased government funding toward clean energy solutions and the introduction of a carbon tax in the U.S.

The most encouraging takeaway from the IPCC report is that there exists a path to keeping the global temperature increase to below 1.5°C, through both aggressive reductions in CO2 emissions as well as carbon sequestration to achieve “net zero” by 2050. In recent days, major corporations including McDonald's Corp. and industry groups such as the International Air Transport Association have made a public commitment to this goal.

In the United States, President Biden is currently targeting an outsized investment to fight climate change. His proposed $3.5 trillion spending plan includes tax incentives for clean energy and electric vehicles, investments to transition the economy away from fossil fuels and toward more wind and solar power, and the creation of a civilian climate corps.

As I research investment opportunities to address this challenge, most of my attention has been directed toward existing ecological and technological opportunities to capture and store carbon. My recent areas of focus include the financial and incentive systems impacting the U.S. agriculture industry, emerging agricultural technologies to measure and sequester carbon in soils, and existing and developing opportunities in direct air capture. I welcome any conversations with investors, founders, and thought leaders with knowledge in these areas.

Economic & Market Update

At this time last quarter, I compared the state of the economy and markets to 2020. I highlighted the above-average economic growth we were experiencing as a result of the easing of COVID-related mobility restrictions globally.

Since then, a number of new risks have emerged, including a rise in COVID cases globally, a higher likelihood that the Federal Reserve will withdraw economic stimulus before year- end, a litany of proposed tax increases, and an increased risk of a U.S. government default resulting from a deadlock in Washington regarding the debt ceiling.

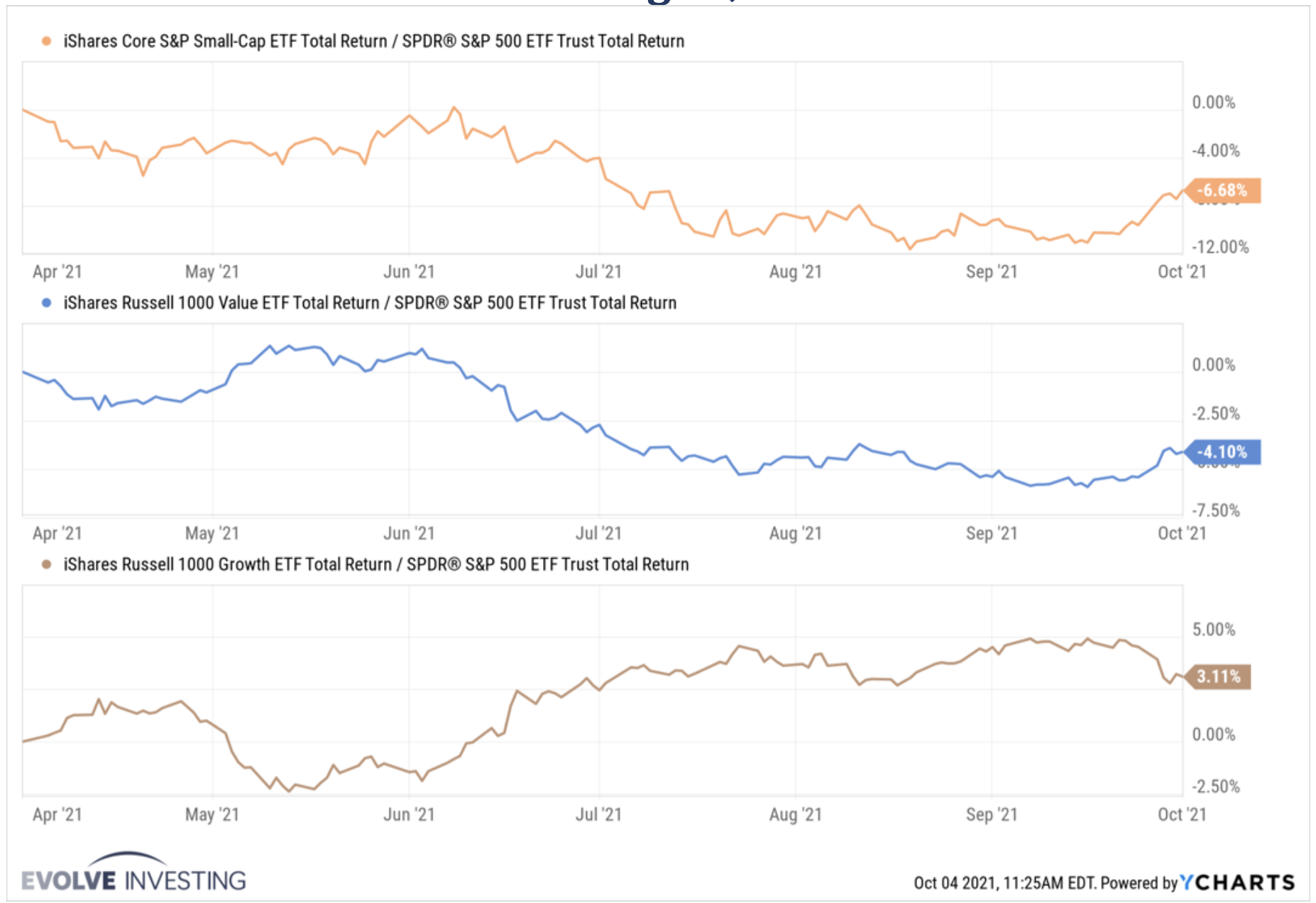

Those who follow my weekly calls know that in today’s environment I tend to favor value stocks over growth stocks, and where appropriate smaller cap stocks for my clients’ portfolios. Starting in September 2020, small cap and value strategies started to outperform, and this trend continued into the spring of 2021.

However, as the aforementioned risks were priced into the market, there was pressure on stocks across several sectors, particularly those that are more cyclical in nature. Small cap and value strategies underperformed as investors moved out of these categories and into large cap technology stocks that are perceived as more COVID-resistant.

As shown in the graph below, over the last month, that trend has reversed course. Long- term bond yields increased following the announcement that the Federal Reserve may start to taper stimulus. As a result, large-cap stocks – including major technology stocks such as Apple Inc., Microsoft Corp., Amazon.com Inc., Alphabet Inc. and Facebook Inc., which together are 22.9% of the S&P 500 – began to sell off. In September, the S&P 500 ended the month 4.8% lower, its first monthly drop since January and the biggest since March 2020.

After reviewing COVID case and hospitalization data, I believe that the Delta wave has peaked, and view the recent economic pullback as temporary. I anticipate that economic growth will continue in coming quarters, albeit at a slower pace than originally expected, and that starting in 2022, we’ll see the Federal Reserve move closer to raising interest rates. These central bank actions will likely lead to rising treasury yields.

Importantly, the performance of value stocks relative to growth stocks tends to be correlated with the steepness of the yield curve, defined as the yields on longer-term bonds relative to short-term bonds. Generally, the yield curve tends to steepen during economic expansions. As long-term interest rates increase, growth stocks can often come under pressure as the cash flows of these companies are generally more heavily discounted.

Despite the risks impacting the market, I believe that we are in the midst of an economic recovery, and I continue to prefer small cap value stocks because this category contains more cyclical, economically sensitive companies that tend to perform well when recessions – and the associated risks of bankruptcy – begin to ease.

At Evolve Investing, nearly all of our clients have a long-term investment horizon, which enables us to capitalize on long-term opportunities. Relative to growth stocks, value stocks are incredibly cheap, with discounts at near-historic highs. The majority of our strategies take into account this opportunity, while also overweighting the companies that are focused on healing our planet, improving our health, and promoting equality.

In the coming days, you’ll receive your quarterly impact reports, which outline your financial performance as well as how your portfolio compares to market benchmarks with respect to the investment causes you’ve selected. Thank you for your continued support and confidence in Evolve Investing.

Best,

Peter Hughes, CFA