3Q23 Letter: "Expectations Management"

To get our market insights delivered directly to your inbox, sign up here.

Business Update

During the third quarter of 2023, Evolve Investing continued its growth trajectory. Our assets under management increased by 7% from the end of last quarter, to an all-time high.

In August 2023 JoeAnna Patterson joined our team. JoeAnna adds over 15 years of experience in the financial sector, in the private wealth management division at Merrill Lynch, at multiple hedge funds, and with several teams at various investment advisory firms. In her full-time role of Senior Client Service Associate, JoeAnna will be co-managing operations and directly supporting our clients with respect to both investment management and financial planning.

The volatility experienced in the third quarter reflects an uncertain monetary policy and economic environment. As your advisor, my goal is to help you navigate short-term challenges while focusing on your long-term goals for wealth creation. Please reach out to me directly anytime to discuss the markets and your investments.

A Tough September

After a solid 2023 rally, stocks had a very challenging September, driven largely by an unexpected surge in interest rates. The S&P 500 was down 4.9% for the month and 3.6% the quarter, whereas the Nasdaq 100 declined 5.8% for the month and 4.1% for the quarter.

The direction and magnitude of movements in Treasury yields can have a significant impact on the prices of stocks and other risk assets. U.S. Treasuries are often perceived as close to “risk-free”, so when the “risk-free rate” increases, so does the opportunity cost of owning stocks, corporate bonds, and other riskier assets. To the extent investors can receive a higher return by purchasing “risk-free” assets, more risky assets become less appealing.

A year ago, the 10-year Treasury yield – the benchmark measure of the “risk-free rate” – hit a local peak of 4.5%. As of mid-summer 2023, when the S&P 500 was up about 18% year to date, it seemed like that peak in Treasury yields wouldn’t be retested, especially following the Fed’s efforts to enhance liquidity following regional bank failures earlier this year.

However, this expectation changed quickly in September, when 10-year Treasury yields surged past 4.6%. The major catalyst behind the spike was the Federal Reserve’s FOMC meeting, during which Jerome Powell stated that the Fed is “prepared to raise rates further if appropriate, and we intend to hold policy at a restrictive level until we’re confident that inflation is moving down sustainably toward our objective.”

10 Year Treasury Yield, Last 10 Years

The takeaway from Powell’s comments is that in light of an economy that continues to run a bit hotter than expected, the Fed needs to leave rates higher for longer to achieve its objectives. As the “higher-for-longer” narrative sets in, investor hopes for lower rates in 2024 are fading, and equity market valuations are fading along with them.

Megacap Tech Continues to Outperform

In last quarter’s letter, I pointed out that the impressive S&P 500 gains experienced in the first half of 2023 were largely driven by a small basket of megacap technology stocks including Tesla (TSLA), Nvidia (NVDA), Meta Platforms (META), Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL), and Amazon (AMZN).

In 3Q23 this trend continued, with the “Magnificent Seven” largely holding gains while other market segments trended lower. The outperformance of megacap technology stocks is most stunning when compared to small cap stocks; the Russell 2000 small-cap index is now down for the year, whereas the “Magnificent Seven” are up 30-200%.

Performance of Big 7 Tech Stocks vs. S&P 500

It’s important to note that when taking into account earnings growth, a core fundamental driver of stock valuations, the outperformance in megacap technology stocks appears justified. As shown in the graphs below, in 2023 earnings expectations have risen steadily for the Nasdaq 100, whereas expectations for the small cap companies in the Russell 2000 are down roughly 25%.

Russell 2000 and Nasdaq 100 2023E EPS Estimates, Year-to-Date

Nonetheless, what’s particularly interesting about this outperformance is that the market is seeming to shrug off two major risk factors facing Big Tech:

First, many megacap technology companies have been viewed as “long duration assets” with the majority of their cash flows - and therefore, their valuations – weighted far into the future. In theory, any unexpected increase in interest rates should have a larger negative impact on megacap tech stocks than other market segments.

Second, major technology companies are again under scrutiny from the U.S. government for unfair anti-competitive practices. In late September the Federal Trade Commission filed a lawsuit accusing Amazon of monopolistic practices that hinder competition and increase prices for its customers.

The 2023 rally reminds me of early to mid-2020, when investors flocked to megacap technology stocks as “safe havens.” The appeal of these larger companies is that they are well established and diversified, with strong balance sheets and competitive market positioning. With these types of companies leading the market and more speculative stocks lagging, my sense is that investors generally remain cautious.

Current Expectations and Outlook

As I consider the outlook for 4Q23 and beyond, I again come back to the questions of (1) what expectations are priced into markets today, and (2) do I foresee any differences in outcomes relative to these expectations?

At the time of this writing, 10-year yields are north of 4.7%, well above last year’s peak, and some Fed officials have signaled that one more rate hike is probably necessary. The market has recently sold off as investors have come to the realization that the Fed is serious about keeping rates higher for longer, thus reintroducing the risk of a harder landing for the economy. Strategists at Goldman Sachs, Morgan Stanley, and JPMorgan have warned that higher rates could lead to further declines in equities.

Given the above factors, my sense is that meaningful negative sentiment is “priced in” to market valuations. The baseline expectation seems to be that Treasury yields will continue to march higher, thus pressuring equities.

However, it’s worth examining recent history to see the relationship between market prices, Fed policy, and interest rates. Below is a graph of the 10-year Real Treasury Rate - which is the 10-year Treasury yield adjusted for inflation - compared to the S&P 500 over the last 20 years. While there appears to be a clear inverse relationship between real rates and equity market performance, one anomaly that jumps out to me is 2013.

10 Year Real Treasury Rate and S&P 500 Level, Last 20 Years

In May 2013 the Federal Reserve announced that it was ending its quantitative easing program, which led to a spike in real interest rates. Within weeks, the S&P 500 fell 8% and the 10-year Treasury yield increased to 3% from 2%. Later that year, in response to the market volatility, the Fed decided not to taper its bond purchases as soon as originally anticipated. Following this shift to a more dovish policy, global stocks continued to advance, and the S&P 500 ended the year up 30%.

The takeaway from the above example is that Fed policy can shift and change in response to multiple factors, including a spike in Treasury yields. As recently as August 2023, Federal Reserve Bank of New York President John Williams suggested that a rate cut could come as soon as 2024 or 2025 in the event that inflation continues its downward trajectory. With inflation well below peak and borrowing costs higher compared to a year ago, a shift to more dovish policy in the near-term is not out of the question.

How We’re Positioning

Last quarter I shared that most of our strategies were currently underweight stocks relative to other assets. At the time, my strategies reflected a bias toward managing downside risk. However, I continued to hold equities across nearly all of my clients’ portfolios, with core positions in Tesla (TSLA), Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL), and Amazon (AMZN).

Relative to last quarter, my bias toward managing downside risk is unchanged. Across my portfolios, I’m holding a lower proportion of stocks relative to my clients’ overall level of risk tolerance. I’ve recommended a higher proportion of fixed income securities, with a preference for floating rate loans and higher-quality corporate bonds, as well as short-duration U.S. government securities.

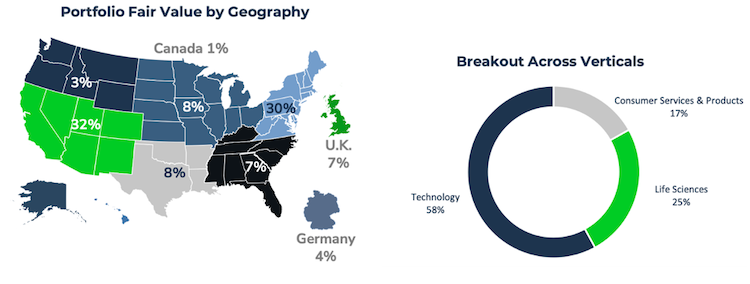

An ideal example of an appropriate investment for today’s environment, in my view, is Runway Growth Finance Corp. (RWAY). Runway Growth manages a diversified portfolio of loans to late- and growth-stage companies across multiple industries and geographies. It is well-diversified, with 99% of its assets in first lien senior secured loans that are collateralized by the underlying assets of the companies.

Runway Growth Finance Corp. Portfolio Overview

Because the loans its portfolio are 100% floating rate, Runway Growth generates higher income and earnings per share in a period of rising interest rates. The dividend yield for RWAY is over 13%, representing the high interest income on the underlying loans. Because of this large income component, I tend to target RWAY for my clients’ tax-deferred accounts, and it has been a core holding for most of 2023.

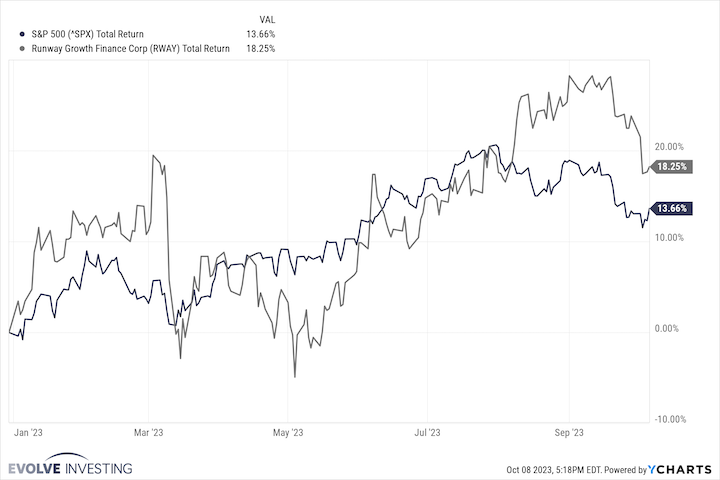

On a year-to-date total return basis, Runway Growth Finance Corp. (RWAY) has outperformed the S&P 500. This outperformance is notable as RWAY carries in my view lower overall risk relative to stocks, primarily because 99% of the loans in its portfolio are secured by the assets of the companies to which it lends.

Runway Growth Finance Corp. vs. S&P 500 Year-to-Date Total Return

Final Thoughts

The third quarter was sobering for most investors, as expectations for a near-term bullish pivot in central bank policy were dashed. Investor sentiment and expectations currently remain low. In order for this market to turn around, we’ll need to see a shift in Fed policy to a more dovish stance, catalyzed by moderating inflation – including wage inflation – and a slowdown in economic activity.

Given this environment, I have recommended that my clients’ take below average risk in their portfolios, with a lower proportion of equities and a higher proportion of fixed income investments including senior secured loans and corporate bonds.

Please reach out anytime to discuss any of the above themes and how your portfolio is positioned. And as always, thank you for your continued support and confidence in Evolve Investing.

Best,

Peter Hughes, CFA, CEPA®