3Q24 Letter: "Stick the Landing"

To get our market insights delivered directly to your inbox, sign up here.

Business Update

During 2024, Evolve Investing increased the number of households we serve, and grew our assets under management by more than 30%. We anticipate that this trajectory will continue into 2025, and are currently evaluating opportunities to expand our team and enhance our service offering.

Can the Fed Stick the Soft Landing?

Following the increase in inflation post-COVID, investors have been squarely focused on whether or not the Federal Reserve can achieve the legendary “soft landing”: a scenario in which inflation moderates to reasonable levels without sacrificing economic growth.

Last month Federal Reserve officials announced their first reduction in the effective funds rate in four years. The Fed cut rates by 0.50%, more than economists expected. (Estimates were split between a 0.25% and 0.50% cut).

Since the late 1970’s, the Fed has had two major objectives: maximum employment and stable prices. When the Fed lowers the effective funds rate, it stimulates economic activity, which tends to drive both employment and prices higher.

So why the larger rate cut relative to expectations? In my view, there are two factors that drove the Fed’s decision:

First, the Fed doesn’t want to be late to enact policy changes, as it appeared to be in 2022. There are generally long lags – as much as 12-18 months - between changes in interest rates and changes in inflation. My sense is that the Fed believes that inflation is under control, and that it will approach its 2.0% long-term goal in the near-term.

Second, the Fed is increasingly concerned about the labor market. In its economic projections released last month, Fed officials forecast that upside risks to the unemployment rate increased meaningfully. By choosing a larger cut to begin this cycle, Fed Chair Jerome Powell made clear that he will defend the labor market – and therefore the U.S. economy - at all costs.

Based on the recent data, it seems plausible that the Fed can achieve its soft-landing goal. Last Friday’s jobs report was stellar, as the unemployment rate fell for a second month in a row, to 4.1%. Inflation, as measured by the Fed’s preferred personal consumption expenditures (PCE) price index, has decreased from a peak of 7.1% in June 2022 to 2.2% in August 2024. And economic growth remains solid, with U.S. gross domestic product up 3.0% y/y in 2Q24.

Like the Fed, I am closely watching the labor market, which in theory should weaken over the next year. If the unemployment rate remains in a healthy 3-5% range over the next 12-18 months, we can pop the champagne and celebrate the soft landing.

However, if unemployment increases into unhealthy territory, then we risk a very challenging scenario: the Fed overshoots on rate cuts to save the labor market, which in turn drives inflation higher. This downside scenario is particularly relevant today, as escalating tensions in the Middle East and port strikes have driven oil prices higher, thus increasing inflationary pressures.

Current Market Expectations and Outlook

Historically, stocks have performed well during rate-cutting cycles. There are fundamental reasons for this performance. As the cost of borrowing declines for publicly-traded companies, capital investments become cheaper, and more dollars flow to the bottom line, supporting their earnings.

S&P 500 one-year performance following first in series of rate cuts

As markets have priced in the soft-landing scenario, major indices have rallied to all-time highs, which has raised some concerns about stretched valuations. Specifically, S&P 500 stocks are trading at 23.2x their projected earnings over the next 12 months, compared with the five-year average of 19.5x and ten-year average of 18.0x.

S&P 500 Current and Projected Price to Earnings Ratio

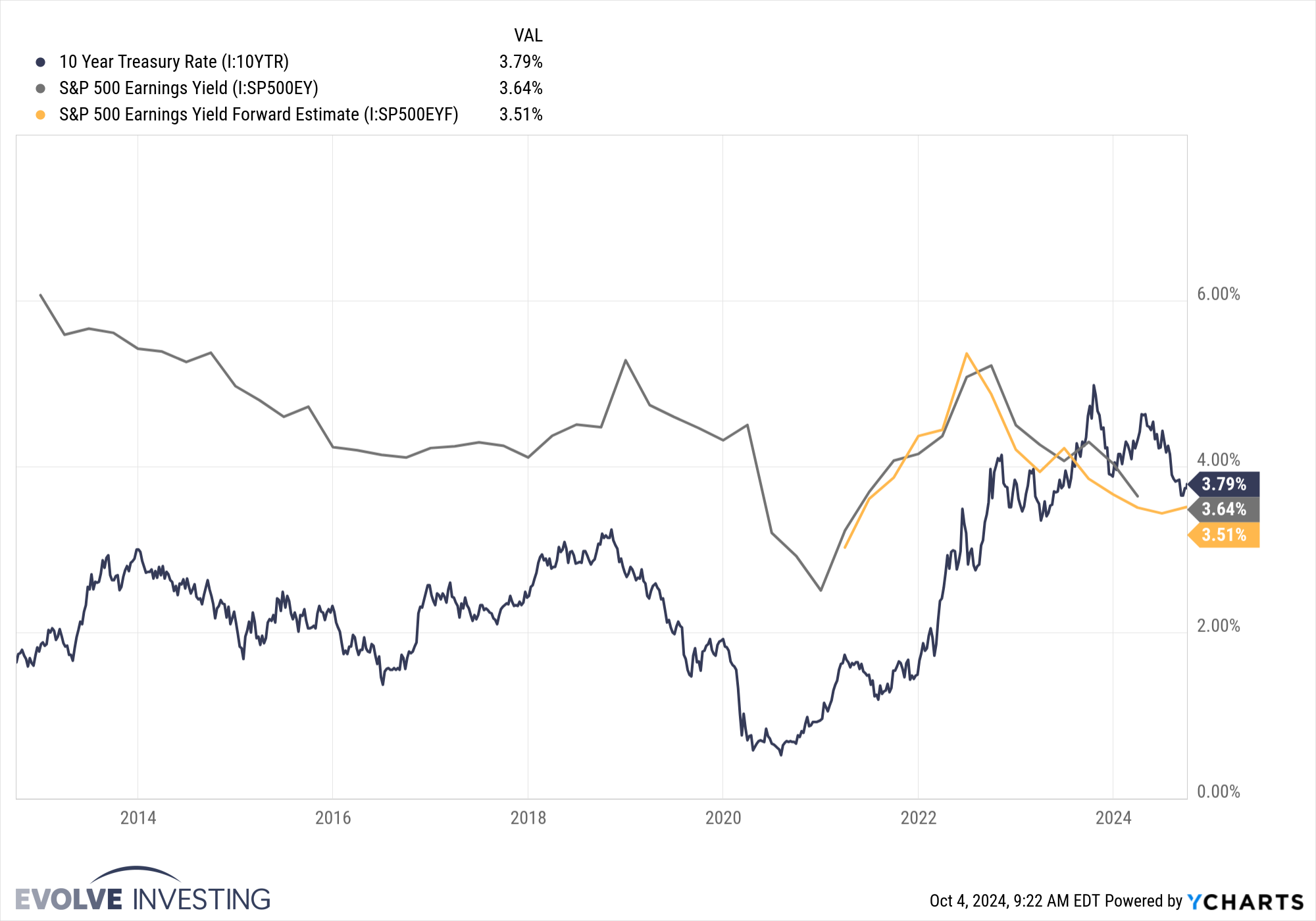

Relative to fixed income securities, equities are more overvalued today than they have been in years. The equity risk premium, which compares the S&P 500 earnings yield to the 10-year Treasury yield, turned negative earlier this year, for the first time in over 20 years. With bonds looking more relatively attractive, I expect equities to be increasingly sensitive to changes in interest rates.

10 Year Treasury Yield vs. S&P 500 Earnings Yield

As valuations stretch, the likelihood of an equity market correction does as well. A correction could be triggered by a negative surprise to economic data – such as a poor jobs number – which could lead to changes in policy decisions as I mentioned above. In the near-term, we could also see an increased focus on risks already weighing on the market, such as the upcoming election or Middle East unrest.

How We’re Positioning

With the Federal Reserve’s rate-cutting path now in place, I expect interest rates to trend downward in the near-term, which should generally be supportive for equities. The aforementioned benefit of lower borrowing costs is particularly clear for small-cap companies, which tend to have a higher percentage of floating-rate debt, as well as a greater dependence on supportive capital markets to refinance upcoming debt maturities.

Over the last quarter, I’ve had conversations with clients about the stretched valuations of megacap technology companies, and in some cases, we have reduced exposure to this sector. Where appropriate, I have increased allocations to small-cap stocks. For households focused on capital preservation, I’ve purchased single-name corporate bonds in order to lock in higher current yields. Any investment decision takes into account each household’s unique investment time horizon, risk appetite, and the potential tax implications of our trades.

The major downside scenario for stocks, in my view, is a deterioration in the labor market, which increases both the risk of recession, and the risk of a policy change that could impact the inflation trend. I believe these risks can be mitigated through sound monetary policy, and will be closely watching the FOMC policy meeting early next month. As long as the U.S. economy remains strong and inflation continues to cool, we should continue to see a supportive environment for all risk assets.

On a risk-adjusted basis, fixed income securities are looking increasingly attractive, in my view. As I mentioned last quarter, I expect the lower rate path to benefit fixed income over a longer-term time horizon, and several of my portfolios contain investment grade and high yield corporate bonds as well as venture debt.

Please reach out anytime to discuss any of the above themes and how your portfolio is positioned. And as always, thank you for your continued support and confidence in Evolve Investing.

Best,

Peter Hughes, CFA, CEPA®